Key judgment

In the GTA, the better question is not whether freehold is always better than condo apartments. The better question is what job each property type is supposed to do in a portfolio.

Detached, semi-detached, and townhouse exposure should be the core allocation because it is tied to land-constrained, ground-level housing. Condo apartments can still have a role. They can diversify the portfolio, and they can outperform in certain windows, but they are more tactical because they are more sensitive to supply cycles, investor demand, and buyer confidence.

Across the complete January 1996 to May 2026 window, ground-oriented housing delivered a stronger return per unit of volatility than condo apartments. The long-term story is clear. Freehold is the core. Condo apartments are the diversifier.

1. The fifty thousand foot view

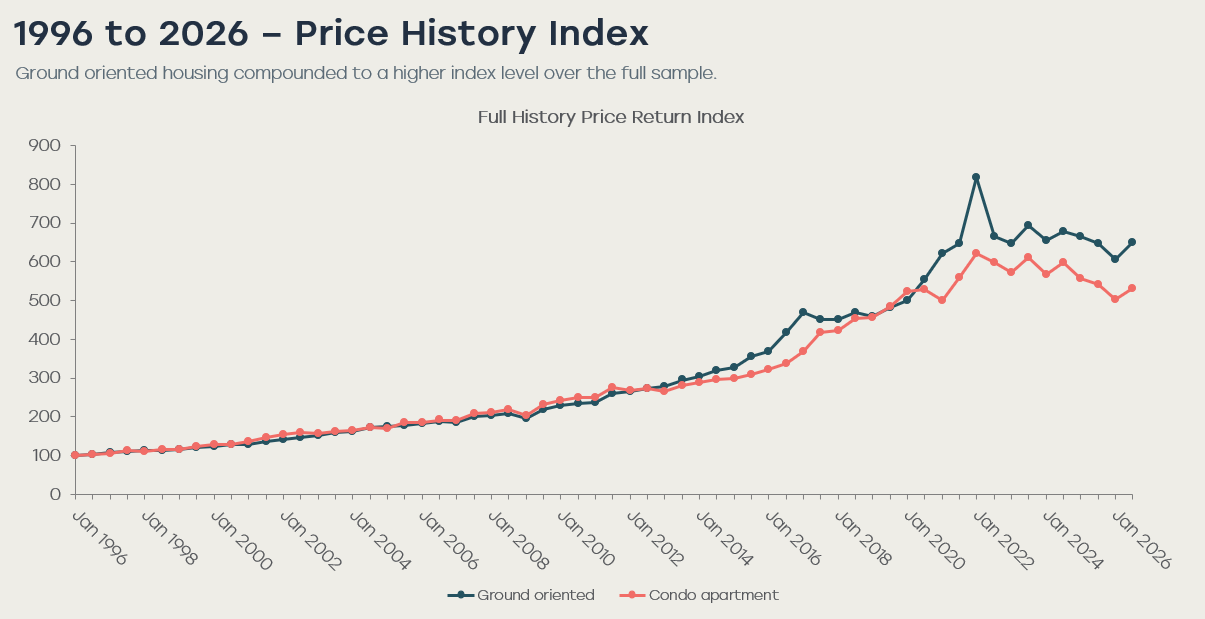

To start, it helps to take a fifty thousand foot view. How has freehold performed relative to condo apartments over the last 30 years?

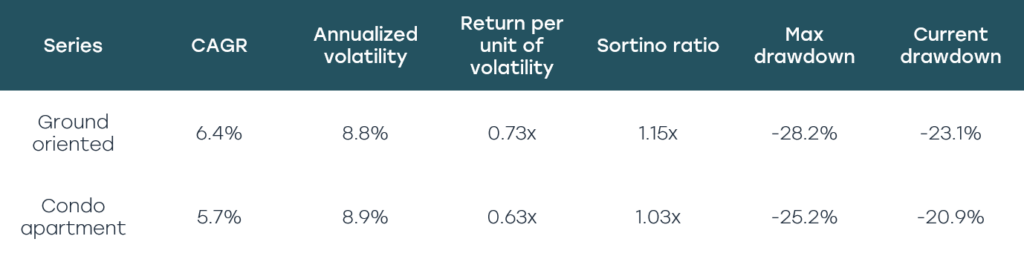

Across the complete January 1996 to May 2026 window, ground-oriented housing delivered a 6.4% compound annual return with 8.8% annualized monthly return volatility. Condo apartments delivered a 5.7% compound annual return with 8.9% volatility. Put simply, for the same amount of risk, ground-oriented housing provided a better return.

The above data is from the uploaded TRREB Market Watch full history workbook. The main comparison uses a ground oriented composite built from detached, semi detached, and townhouse monthly returns, and compares it against condo apartments.

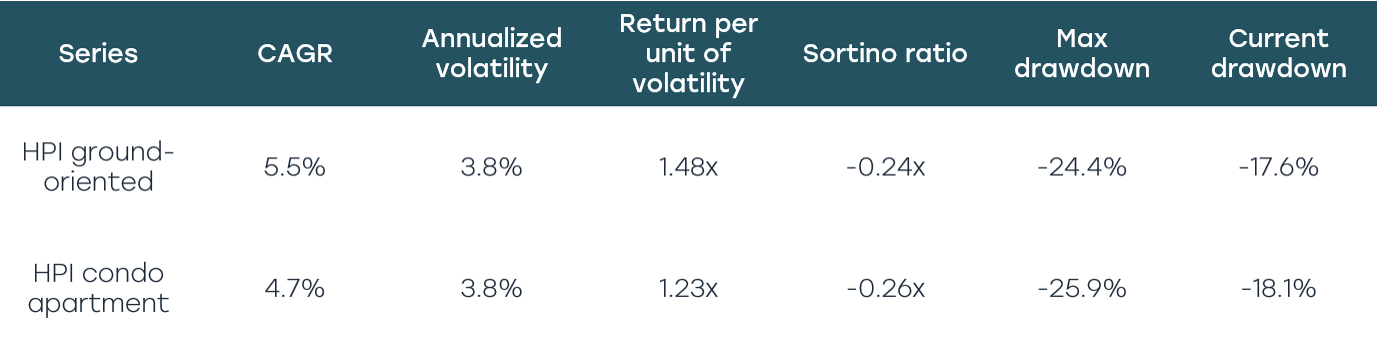

Using MLS HPI data gives a similar cross-check. The HPI series in the updated workbook begins in January 2005 and runs through May 2026. Over that period, the HPI ground-oriented composite produced a 5.5% compound annual return and a 1.48x return per unit of volatility. Condo apartments produced a 4.7% compound annual return and a 1.23x return per unit of volatility. The point is the same: the more apples-to-apples HPI series still supports the view that ground-oriented housing produced better return per unit of risk than condo apartments.

2. What happened in 2017?

Real estate is a highly regime dependent asset class. It depends on local supply and demand economics, and different property types can outperform in different periods.

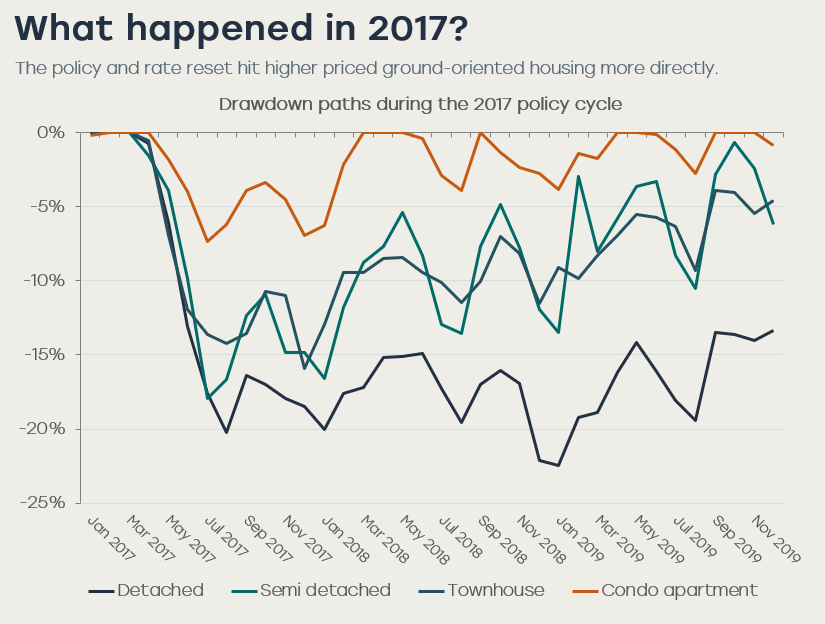

The 2017 cycle is the best example. It was a policy, rate, and affordability shock that hit higher priced ground oriented housing more directly. Ontario announced the Fair Housing Plan in April 2017, OSFI finalized the revised B 20 mortgage underwriting guideline that came into effect on January 1, 2018, and the Bank of Canada later described tighter mortgage qualification rules and higher interest rates as weighing on mortgage activity.

Because the shock was concentrated in more expensive and more rate sensitive segments, condo apartments experienced a smaller drawdown during the 2017 to 2019 policy cycle. Condo apartments fell -7.3%. Detached fell -22.5%, semi detached fell -17.9%, and townhouse fell -15.9%.

This period is an important reminder to consider diversification in a real estate portfolio. Certain property types can be more exposed or sensitive to specific policy events. Having condo apartments in the portfolio during this period would have reduced the overall drawdown.

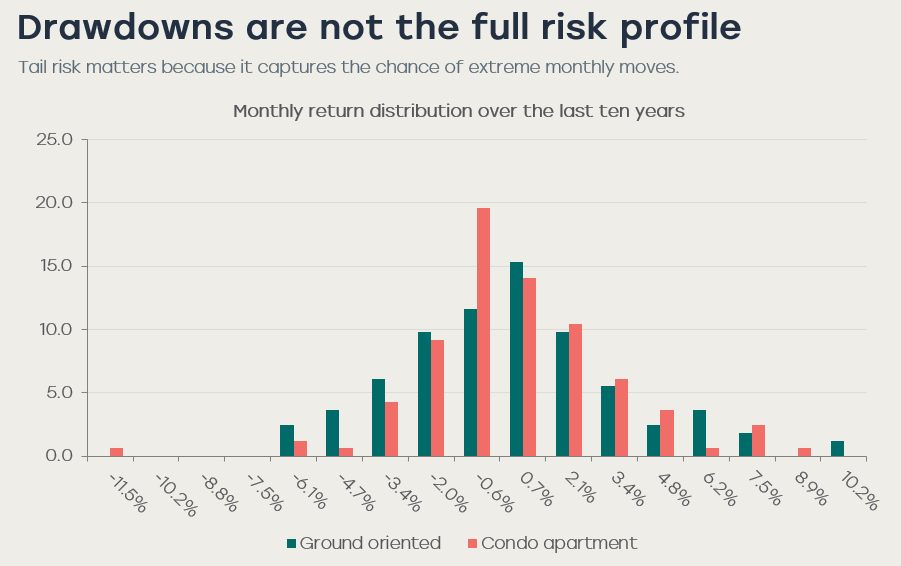

3. Drawdowns are not the full risk profile

Drawdowns are important, but they are not the only way to look at risk. Kurtosis measures how much of the return distribution sits in the tails. In simple English, higher kurtosis means more of the action comes from unusually large moves rather than normal monthly changes.

Over the last ten years, condo apartments had higher excess kurtosis than ground oriented housing. Condo apartment excess kurtosis was 2.15 compared with 0.35 for ground oriented housing. This means condo apartments had fatter tails in monthly returns.

Why does that happen? A likely reason is supply. Condo apartment supply can come online in larger waves because developers can add hundreds of units in one project. Ground oriented supply is harder to add because it needs more land. When demand is strong, condos can work very well. When demand weakens at the same time that completions arrive, the price reaction can be sharper.

The implication is that max drawdown does not provide the full risk profile for any asset class. It is important to understand the distribution of returns and what that means for that property type. The higher excess kurtosis for condo apartments means that they are more susceptible to extreme outcomes in the real estate cycle.

There is evidence of this in the current cycle. Financial Post described a new condo market that had hit bottom as sales fell, and Mortgage Professional America reported that some preconstruction condo buyers were facing appraisal gaps after values fell below contract prices.

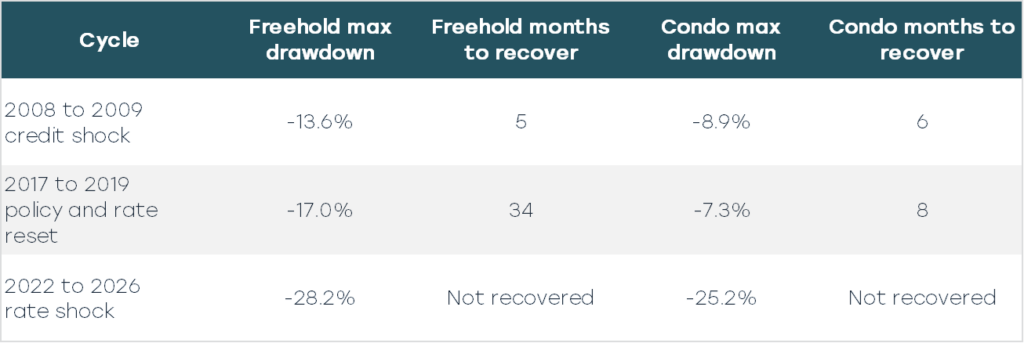

4. Recovery after drawdown

Another metric to evaluate when comparing asset classes is recovery after a drawdown. The question is not only how far prices fall, but how long it takes to get back to the prior peak.

The recovery table shows why the answer is not one dimensional. Condo apartments recovered faster after the 2017 policy cycle because the shock was aimed more directly at higher priced ground oriented housing. In the 2022 rate shock, both segments are still below their prior peaks.

The broader lesson is that recovery speed depends on what caused the drawdown. When policy hits affordability in expensive housing, condo apartments can help. When the condo market is dealing with excess supply and weaker investor demand, condos can carry more tail risk.

5. Supply is the structural difference

Ground oriented housing is limited by supply, while condo apartment supply can adjust more quickly. This is the structural difference between the two asset classes.

The current supply context reinforces the point. In the first quarter of 2026, CREA and TRREB reported 5.4 months of inventory for condo apartments compared with 4.2 months for single detached homes and 2.5 months for semi-detached homes. Condo apartments also had a longer median days on market at 34 days compared with 21 days for single detached and 17 days for semi-detached.

The supply issue is also visible in Toronto. During the current cycle, condo apartment supply arrived as rates rose and investor demand weakened. Mortgage Professional America reported that completed condo units in the Toronto and Hamilton area reached a record 29,800 in 2024, with 30,793 units expected in 2025. The article also noted that growing supply placed downward pressure on values.

The investment implication is straightforward. Condo apartments can work, but entry point and supply timing matter more. Ground oriented housing is not risk free, but the supply response is slower because land is scarce and new ground oriented housing is harder to create at scale.

6. Real estate is cycle dependent

The early 2000s matter because they show that condo apartments can lead. From January 1996 to December 2001, condo apartments compounded at 7.1% per year compared with 5.8% for ground oriented housing. This was a catch up period from a lower price base when affordability was easier and the condo market had room to rerate.

Ground-oriented housing led in most later cycles. It led during the 2002 to 2008 expansion, the 2008 to 2012 recovery period, the 2013 to April 2017 boom, and the 2020 to February 2022 pandemic cycle. Condo apartments led during the 2017 to 2019 policy cycle because they were less exposed to the affordability shock facing higher priced freehold properties.

This is the key portfolio point. You never know with certainty which cycle you are in. Ground-oriented housing has been the stronger long-term core allocation, but condo apartments have still helped in certain regimes. That is why diversification matters.

Conclusion

In summary, ground oriented housing provides a better return per unit of risk for most participants in the residential real estate market. It also protects investors against periods of over and under supply in the condo market.

However, real estate is a regime dependent asset class. Different property types respond differently to economic changes, government policy, interest rates, buyer demand, and supply. Therefore, it is prudent to have both condo apartments and freehold properties in the portfolio.

The role of each should be different. Ground oriented housing should be the core. Condo apartments should be used as diversification and as a tactical allocation when pricing, supply, and demand conditions are attractive.